Inside Automated Deduction Frameworks: How Verification Protocols Protect Service Subscriptions in Virtual Marketplaces

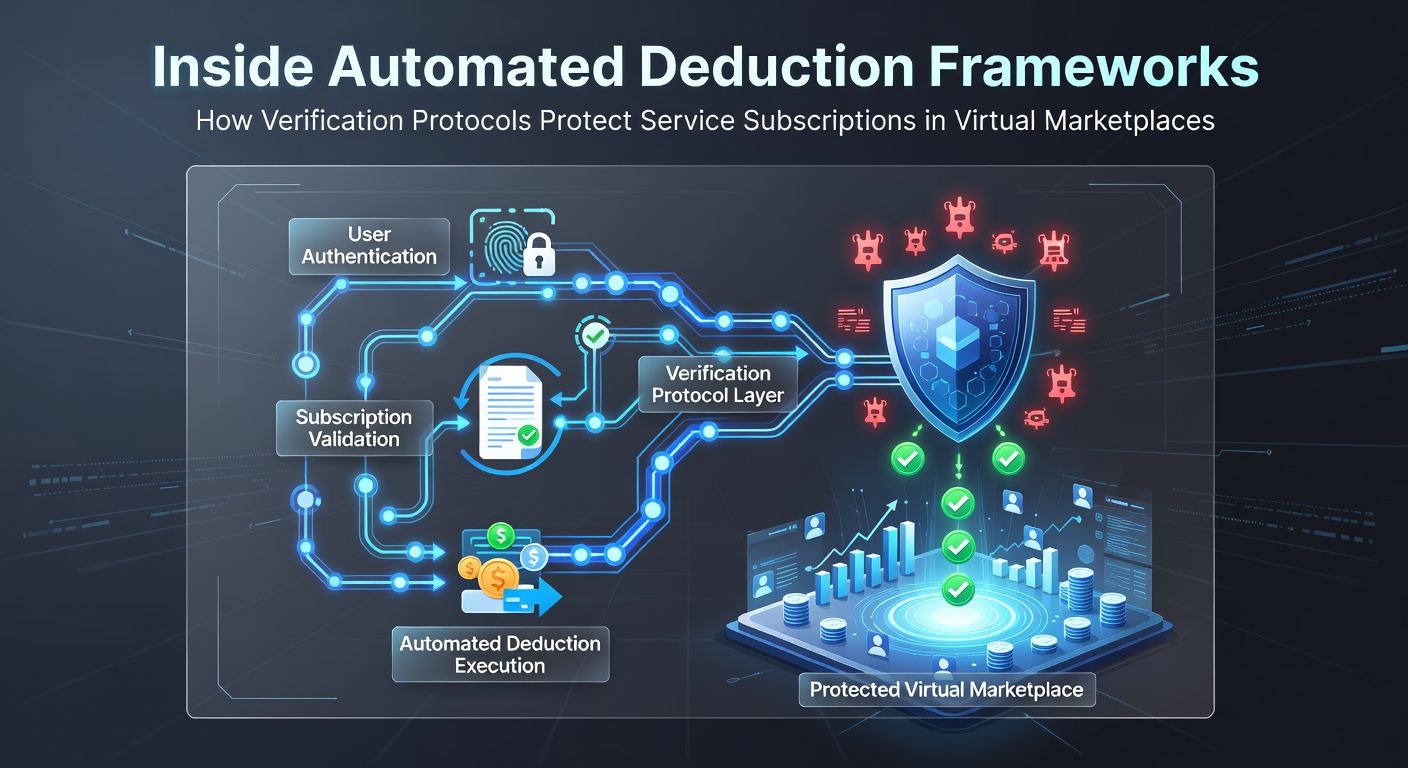

Automated deduction frameworks handle recurring charges for digital services across virtual marketplaces while verification protocols operate at multiple layers to confirm transaction legitimacy before funds move. These systems combine rule-based checks with machine learning models that analyze transaction patterns in real time, and they operate continuously without manual intervention for each billing cycle. Data from industry reports shows that such layered approaches reduce unauthorized deductions by filtering out anomalies during the authorization sequence.

How Automated Deduction Systems Process Recurring Payments

Service providers in virtual marketplaces rely on automated deduction frameworks to pull subscription fees on scheduled dates, and these frameworks integrate directly with payment processors that route requests through established networks. The process begins when a stored credential triggers a deduction request, after which verification protocols evaluate merchant identifiers, amount consistency, and historical subscriber behavior before approving the transfer. Observers note that this sequence prevents many forms of account takeover because mismatched data points halt the transaction at the earliest stage.

Token references replace actual card details in most modern setups, yet verification still occurs through dynamic signals such as device location, IP reputation, and velocity of prior attempts. Research indicates that frameworks incorporating these signals achieve higher approval rates on legitimate renewals while blocking suspicious patterns that emerge during high-volume fraud campaigns. In May 2026 several platforms updated their deduction logic to include additional behavioral scoring drawn from session duration and navigation paths within the marketplace interface.

Core Verification Protocols and Their Roles

Verification protocols function through sequential gates that include address verification services, card security code matching, and three-domain secure challenges when risk thresholds are exceeded. Automated deduction frameworks apply these gates selectively rather than uniformly, which preserves conversion rates on low-risk renewals while escalating scrutiny for accounts showing sudden geographic shifts or unusual device changes. Experts have observed that selective application keeps false declines below thresholds that would otherwise disrupt subscriber retention metrics.

Additional layers incorporate machine learning classifiers trained on historical chargeback data, and these models assign risk scores that determine whether a deduction proceeds automatically or requires secondary confirmation. Figures from payment network analyses reveal that risk-scored transactions experience fewer disputes compared with unfiltered recurring charges, because the scoring step surfaces indicators such as mismatched billing cycles or rapid subscription stacking across multiple merchants.

Integration with Virtual Marketplace Infrastructure

Virtual marketplaces embed deduction frameworks within their account management modules so that subscription status updates trigger immediate verification checks before the next scheduled pull. This integration allows platforms to synchronize user permissions, service tiers, and payment methods in one workflow, and it reduces the window during which compromised credentials might generate repeated unauthorized charges. Those who manage large-scale subscription portfolios report that centralized verification dashboards provide clearer visibility into which accounts trigger repeated protocol interventions.

Marketplace operators also connect these frameworks to external data sources that supply real-time lists of compromised credentials and known fraud rings. When a stored payment method matches an entry on such a list, the deduction request routes through heightened verification that may include out-of-band authentication via email or mobile push notification. According to Bank for International Settlements analysis, marketplaces that maintain active connections to shared fraud databases record measurably lower rates of successful unauthorized deductions over successive quarters.

Regulatory Context and Data Handling Standards

Automated deduction frameworks must align with data protection requirements that govern how subscriber information is stored and transmitted during verification exchanges. In several jurisdictions these requirements mandate encryption standards and audit logging that capture every protocol decision for later review. Canadian regulatory guidance from the Office of the Superintendent of Financial Institutions emphasizes that recurring payment processors document the rationale behind each verification outcome, which supports both compliance examinations and internal model refinement.

Cross-border marketplaces face additional complexity because deduction requests may originate in one region while the subscriber resides in another, and verification protocols must reconcile differing authentication expectations. Research from the University of Melbourne Centre for Digital Transformation shows that frameworks capable of applying region-specific rules within a single processing pipeline maintain consistent protection levels without fragmenting the subscriber experience. As of May 2026, several marketplace operators have begun testing unified policy engines that adjust verification intensity based on the subscriber's registered jurisdiction rather than the merchant's location.

Performance Metrics and Continuous Improvement

Operators track key performance indicators such as approval rate, chargeback ratio, and subscriber retention following verification events to evaluate framework effectiveness. These metrics feed back into model retraining cycles that occur at regular intervals, and the updated classifiers then influence future deduction decisions. Data compiled across multiple virtual marketplaces indicates that iterative refinement of verification thresholds correlates with sustained reductions in fraud losses while approval rates for genuine renewals remain stable.

Monitoring tools also surface edge cases where legitimate subscribers trigger elevated risk scores because of travel or device upgrades, and automated systems can route these cases to lighter verification paths once additional context is confirmed. The result is a feedback loop that balances security with operational continuity, and marketplace teams review aggregated outcome data rather than individual transactions to guide further protocol adjustments.

Conclusion

Automated deduction frameworks combined with layered verification protocols form the operational backbone that safeguards recurring service subscriptions inside virtual marketplaces. These systems process high volumes of scheduled payments while applying targeted checks that distinguish routine renewals from fraudulent attempts. Continued evolution of risk models and regulatory alignment supports ongoing effectiveness as transaction patterns and threat landscapes shift over time.